Aweh Dear Ruminants and Groupies,

The Two Capitalisms

There are, it seems to me, two very different forms of capitalism.

In the first, value creation is brutally tested every single day. If you are a dentist, patients return only if you are competent. If you are a surgeon, your reputation rests on outcomes. If you are an architect, engineer, builder, or plumber, clients eventually notice whether what you do actually works. If you pull out the wrong tooth, the market has an unpleasant habit of introducing you to unemployment.

Meritocracy is not an aspiration. It is a survival mechanism.

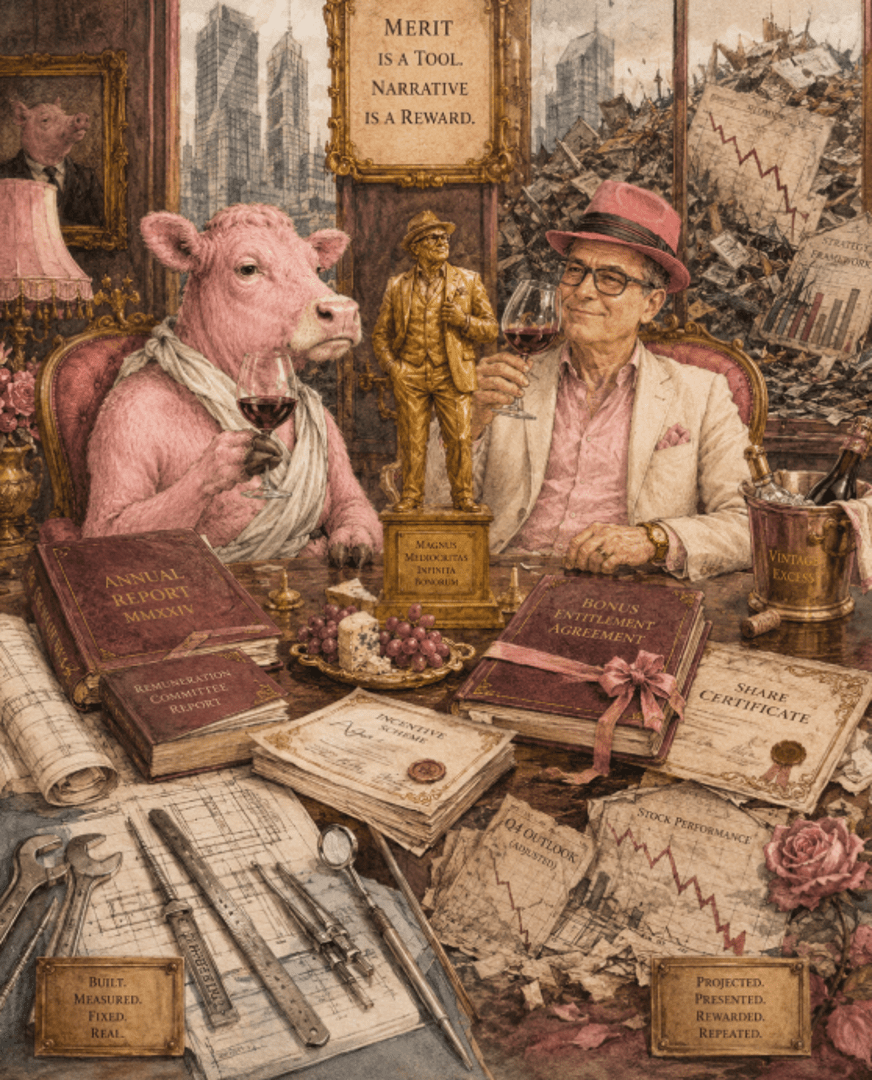

The pink cow nodded. Unlike remuneration committees, cows understand consequences.

The first capitalism is rude enough to notice failure. The second often promotes it, bonuses it, and invites it to speak at Davos.

The second form of capitalism inhabits glass towers, annual reports, and remuneration committee meetings. Here, the connection between value created and rewards received can become wonderfully elastic.

The Great Corporate Fairy Tale

One of the comforting myths of modern capitalism is that listed companies are populated by extraordinary capital allocators and visionary leaders whose fortunes rise and fall in perfect harmony with those of ordinary shareholders.

Every chief executive is introduced as an exceptional visionary.

Every annual report contains photographs of deeply serious people in hard hats pointing purposefully towards the horizon.

Every remuneration report explains that the latest salary increases, bonuses, share options, or long-term incentive plans which are carefully designed to “align management with shareholders” and retain visionary leadership.

It sounds wonderfully fair.

Unfortunately, it is also rather difficult to reconcile with the evidence.

The Man Who Counted

Enter Hendrik Bessembinder.

An academic with the deeply inconsiderate habit of ruining excellent stories using actual data.

His research found that over the long history of the US stock market, roughly four out of every seven listed companies failed even to outperform one-month US Treasury bills.

Even more awkwardly, just 4% of listed companies accounted for all the net wealth created by the US stock market.

Pause for a moment.

If only 4% of companies create essentially all the net wealth, then the overwhelming majority are not the compounding machines annual reports would like us to imagine. A tiny minority become spectacular compounders. A much larger group produces mediocre returns, moves essentially sideways, or fails even to beat cash. A substantial number simply destroy shareholder value.

Which raises an awkward question.

What exactly are all those executives being paid millions, or tens of millions, to achieve?

The Genius Isn’t Where You Think It Is

The extraordinary performance of the S&P 500 does not contradict Bessembinder’s findings.

It explains them.

The S&P 500 has delivered exceptional long-term returns not because all 500 companies are exceptional, but because it is perhaps the greatest Darwinian machine ever invented.

The spectacular winners become larger and automatically receive more of your capital.

The mediocre companies drift quietly into irrelevance.

The failures eventually disappear altogether.

Nvidia, Apple, Microsoft, and Amazon grow to dominate the index.

Yesterday’s corporate visionaries quietly exit through a side door.

The genius, it turns out, is not necessarily in the executives.

It is in the index.

When Natural Selection Doesn’t Work

Individual companies offer shareholders no such elegant escape mechanism.

Corporate history is littered with examples where shareholders suffered catastrophic losses while those responsible remained remarkably employable.

General Electric destroyed hundreds of billions of dollars of market value over two decades.

WeWork vaporised tens of billions of investor capital.

The names change.

The script rarely does.

Exhibit A: Brait

Brait is merely one South African illustration of this much broader phenomenon.

Shareholders watched the company’s share price fall from a peak of around R167 in April 2016 to about R2, while the reported net asset value shrank from R136.27 per share in March 2016 to R3.27 per share in March 2026.

Almost the entire accumulated shareholder value disappeared.

Existing shareholders were then invited, more than once, to inject fresh capital through deeply discounted rights issues to stabilise the balance sheet and rescue whatever remained.

It was rather like being poisoned by a restaurant and then being asked to contribute towards replacing the chef’s stove.

Before the collapse, senior members of Brait’s investment team participated in the controversial Fleet incentive structure.

The investment team collectively acquired approximately 18% of Brait through a highly leveraged share scheme. Much of the original purchase was financed by Brait, with the debt subsequently refinanced by banks under an indemnity provided by Brait.

When the share price climbed towards R167, the participants’ stake had an enormous gross market value, and they stood to become spectacularly wealthy.

When the share price collapsed, the pledged shares no longer covered the borrowing. The Fleet bank loan was ultimately recognised on Brait’s consolidated balance sheet. By March 2018, the loan stood at approximately R1.91 billion, while the pledged Brait shares were worth only about R1.26 billion.

A significant part of the financing problem had therefore migrated back to Brait and its shareholders, as financial sewage so often does.

Heads, management participated generously in the upside.

Tails, shareholders helped clear away the wreckage.

Perhaps that is the most unsettling aspect of the entire episode. Nothing in this story requires villains. Ordinary incentives, perfectly legal contracts, and conventional corporate governance proved entirely sufficient.

To be absolutely clear, I have found no court or regulatory finding of fraud or unlawful conduct arising from the Fleet structure.

That is precisely the point.

The arrangement did not need to be illegal to be profoundly asymmetric.

The system operated broadly as its structure allowed it to operate: substantial leveraged upside for the investment team, with an important part of the downside ultimately returning to the company.

There may be no proven criminality.

But there is certainly a distinct stink rising from the corporate-governance compost heap.

So, What Does It Actually Take?

Which raises another uncomfortable question.

What, exactly, does it take to become a corporate leader?

We like to imagine that boardrooms are populated by the business equivalents of Olympic athletes, selected through a relentless meritocratic competition because they possess extraordinary gifts for leadership and allocating capital.

Really?

Or perhaps the selection criteria are rather different.

Political skill.

Network building.

Patronage.

Presentation.

Confidence bordering on certainty.

The ability to reassure boards, charm investors, navigate remuneration committees, and survive organisational politics.

If Bessembinder is even approximately right, the average listed-company executive is not a wealth-creating genius. He is an extremely well-paid passenger on a bus whose progress is driven by a handful of engines at the front while the rest consume fuel, wave from the windows, and claim credit for the journey.

They are simply one participant in a system where a tiny minority of spectacular successes masks a surprisingly large number of expensive mediocrities and failures.

Yet nearly all are compensated as though they belong to the exceptional minority.

The Pink Cow Test

Of course, bloggers inhabit the first and rather less forgiving form of capitalism.

Nobody is compelled to read a mediocre blogger, however many pink cows he deploys in support of the argument. There is no remuneration committee to explain that declining readership reflects “challenging market conditions”, no long-term incentive plan for producing the same joke for the seventeenth time, and no rights issue through which loyal readers can be asked to recapitalise the blog.

The meritocracy is refreshingly brutal.

Write something worth reading or disappear quietly into the digital compost heap.

Which may explain why I remain a passionate supporter of meritocracy.

At least until somebody offers me a Fleet scheme for mediocre bloggers with a company guarantee and unlimited upside.

Even a pink cow has principles.

Mostly.

Until next time,

Bruce